Investing as a very contemporary concept can be unnerving for an amateur. Seeing the involvement of real hard-earned money, risk appetite is likely to run low in such cases. To build on healthy investing know-how, it is vital that we educate ourselves about the options and then evaluate the best suited. The golden rule that is adapted from the best financial guides claims, “Returns on Investments should be equal to or exceed (favorable) the Rate of Inflation”. Whilst at it, it would be a good idea to always diversify your investments so that they do not stand a risk all at the same time leading to an impending loss. Following is an insight into the means through which investments can be made.

STOCKS

Popular as equity or share market, stocks are essentially stakes in a publicly-traded company. Therefore, having brought a stock of a public company, you may stand to gain a portion of the profits earned equivalent to the number of shares brought. Investors also receive ‘dividends’, which are effectively a portion of a company’s profit paid out to its shareholders of a few publicly traded companies in their portfolio. Prices of these shares are volatile and are prone to market fluctuations, ergo, a long-term investor is likely to withstand this volatility. The risk to rewards proportion is relatively higher than other modes of investing and requires a concrete analysis.

BONDS

Bonds are investments that classify as fixed income security, which essentially lends your money to the issuer who pays you a periodic fixed interest on the investment made. It is a debt instrument issued by Corporate, Municipal, government or treasury bonds. These are usually issued by the issuer to raise money for capital, for a set period of time.

Bonds are investments that classify as fixed income security, which essentially lends your money to the issuer who pays you a periodic fixed interest on the investment made. It is a debt instrument issued by Corporate, Municipal, government or treasury bonds. These are usually issued by the issuer to raise money for capital, for a set period of time.

PPF

When it comes to planning your retirement objectives, Public Provident funds top the list! Categorized mainly as either Employee Provident Fund or/and Public Provident Fund, your retirement corpus has a head start.

By the book, Provident funds are an obligatory government-sponsored retirement scheme which cumulates the amount cut off from the salary and is paid to the employee in full when/if they resign or retire. The added benefit of income tax benefits and capital safety adds to its case. The interest that you receive on the principal amount at the time of maturity ( lock-in period being 15 years) is entirely tax-free. Talking of instalments to be paid, a flexible system of payments is in place that allows either 12 instalments or a deposit of a lum-sum amount annually. The lock-in period for the PPF is 15 years with a corpus amount available on maturity. Note, that partial withdrawals are allowed from the 6th year.

Sovereign Gold Bonds

Sovereign gold bonds are denominated of gold in grams issued as securities by the government of India (RBI) in series every year. These bonds are a successful substitute for the risk and cost of holding physical gold in addition to saving the “making charges” with assured purity. The investors pay for the bond in cash and are assigned a unit of gold redeemable on maturity at market value along with interest. Even though susceptible to a decline in market price, an investor does not lose on the number of units held by them. The fixed interest rate is 2.50 annually. Interest is credited semi-annually while the last payable interest is given with the Principal amount.

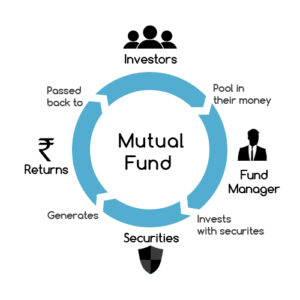

Mutual Funds

This financial instrument requires various instruments to pool the money and invest in securities like stocks and bonds. The returns are based on how the market performs. The instalments can either be made through a SIP or lumpsum. An actively managed mutual fund is overlooked by a manager who picks the stocks for the portfolio.

This financial instrument requires various instruments to pool the money and invest in securities like stocks and bonds. The returns are based on how the market performs. The instalments can either be made through a SIP or lumpsum. An actively managed mutual fund is overlooked by a manager who picks the stocks for the portfolio.